![http://UPSC%20coaching%20in%20India%20-%20Best%20UPSC%20coaching%20institute%20-%20UPSC%20Mentor%20coaching%20-%20UPSC%20preparation%20institute%20-%20IAS%20coaching%20center%20-%20UPSC%20online%20coaching%20-%20Best%20IAS%20coaching%20in%20India%20-%20UPSC%20classes%20for%20beginners%20-%20Civil%20services%20preparation%20-%20IAS%20preparation%20institute%20-%20UPSC%20mentorship%20program%20-%20UPSC%20exam%20guidance%20-%20IAS%20study%20material%20-%20UPSC%20Prelims%20coaching%20-%20UPSC%20Mains%20coaching%20-%20UPSC%20interview%20preparation%20-%20Best%20IAS%20online%20classes%20-%20UPSC%20coaching%20with%20personal%20mentorship%20-%20Affordable%20UPSC%20coaching%20-%20UPSC%20test%20series%20-%20UPSC%20coaching%20near%20me%20-%20Best%20IAS%20coaching%20near%20me%20-%20UPSC%20institute%20in%20[your%20city]%20-%20IAS%20coaching%20center%20in%20[your%20city]%20-%20The%20UPSC%20Mentor%20coaching%20-%20The%20UPSC%20Mentor%20IAS%20classes%20-%20The%20UPSC%20Mentor%20UPSC%20course%20-%20UPSC%20Mentor%20online%20program.](https://theupscmentor.in/wp-content/uploads/2024/11/THE-UPSC-2-e1762319162137.png)

admin

admin

Context / Why this is in news

0.1 India is ending 2025 with stable macroeconomic indicators while preparing for challenges expected in 2026, shaping the India economic outlook 2026.

0.2 Global factors such as US tariffs, trade uncertainty, and structural changes driven by technology and AI are likely to persist.

0.3 A major concern highlighted is weak domestic consumption, which could affect private investment growth.

India’s economic position at the end of 2025

0.1 India closes the year with relatively strong indicators, including low inflation and lower interest rates.

0.2 Economic activity remained steady during October–December, though early signs of softening demand are visible.

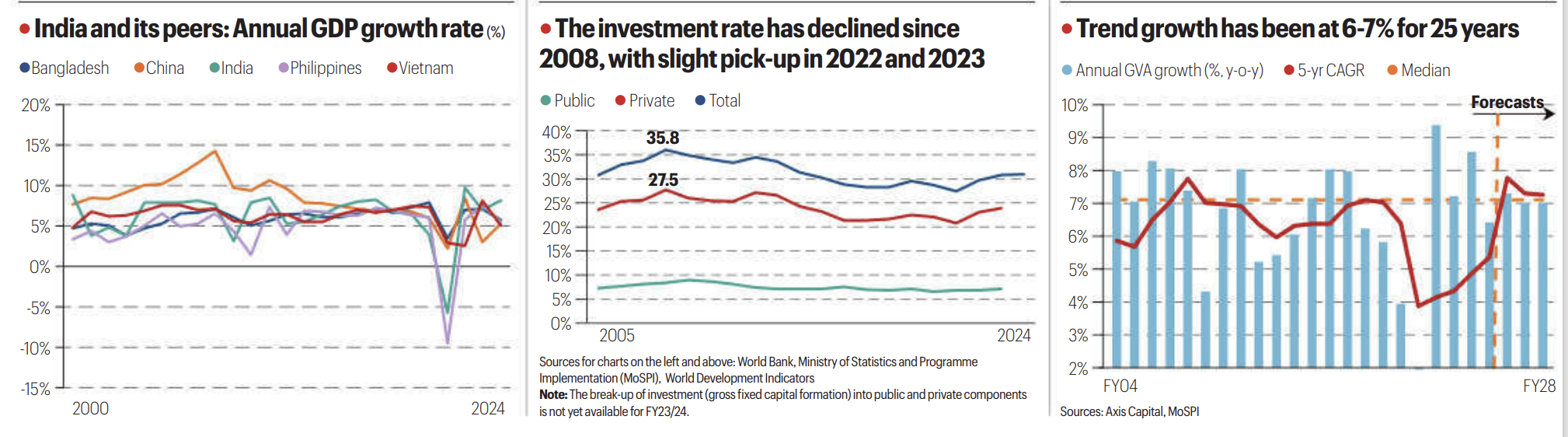

0.3 India remains the fastest-growing major economy, with GDP growth for FY26 expected around 7–7.3%.

Global tariff shocks and uncertainty

0.1 Global tariff shocks continue to influence India’s external environment.

0.2 The US imposed a 25% reciprocal tariff, along with penalties linked to India’s purchase of Russian crude oil.

0.3 Uncertainty over US trade policy complicates export planning and investment decisions.

0.4 Restrictions on Chinese exports may divert excess goods into Asia, Africa, and Latin America, intensifying competition for Indian exporters.

Exports, current account and capital flows

0.1 Exports to the US improved in November, supported by tariff-exempt sectors such as pharmaceuticals and electronics.

0.2 The current account deficit, at 1.3% in Q2 FY26, remains manageable due to services exports and strong remittances.

0.3 Continued foreign investment outflows could complicate financing of the current account.

0.4 Slower corporate earnings and tariff uncertainty may keep foreign investors cautious, particularly in equity markets.

Domestic demand and consumption challenges

0.1 Reviving domestic consumption is critical for sustaining private investment.

0.2 Rural demand remains relatively strong due to good agricultural output and improved rabi sowing.

0.3 Urban demand continues to lag and is recovering slowly.

0.4 Capacity utilisation, at around 75–77%, limits the immediate need for fresh capital expenditure.

Investment trends and reform measures

0.1 Private investment shows mild improvement, supported by higher bank credit growth.

0.2 GST rationalisation and festive season spending supported demand in October–November, though sustainability remains uncertain.

0.3 Policy steps such as labour law reforms, GST changes, and nuclear sector amendments aim to support investment.

0.4 Financial sector reforms, including higher foreign ownership in insurance and changes in banking and pension rules, may attract capital inflows.

Outlook for 2026

0.1 The effects of earlier fiscal and monetary tightening have eased, improving growth prospects for FY26.

0.2 Monetary easing is expected to further support growth in FY27.

0.3 Services exports have strengthened, though tighter visa policies in the US and Europe pose risks.

Core takeaway

0.1 India has managed global tariff pressures so far due to stable macro fundamentals and strong services exports.

0.2 However, weak domestic consumption remains the key risk in the India economic outlook 2026, as stronger demand is essential for a sustained revival in private investment.

![UPSC coaching in India - Best UPSC coaching institute - UPSC Mentor coaching - UPSC preparation institute - IAS coaching center - UPSC online coaching - Best IAS coaching in India - UPSC classes for beginners - Civil services preparation - IAS preparation institute - UPSC mentorship program - UPSC exam guidance - IAS study material - UPSC Prelims coaching - UPSC Mains coaching - UPSC interview preparation - Best IAS online classes - UPSC coaching with personal mentorship - Affordable UPSC coaching - UPSC test series - UPSC coaching near me - Best IAS coaching near me - UPSC institute in [your city] - IAS coaching center in [your city] - The UPSC Mentor coaching - The UPSC Mentor IAS classes - The UPSC Mentor UPSC course - UPSC Mentor online program.](https://theupscmentor.in/wp-content/uploads/2025/11/cropped-THE-UPSC-1.png)